Get Clients MUCH Higher 2021 Tax Deductions Using this Overlooked Strategy

While the Biden administration was unable to pass its massive tax reform legislation through the Build Back Better Plan in 2021, many relieved business owners and financial advisors are given a unique opportunity to focus on tax mitigation strategies. As the potential still remains to pass legislation, in some capacity, it’s important your clients understand their options.

The Setting Every Community Up for Retirement Enhancement Act of 2019, (SECURE Act) has provided a way for business owners to start a profit sharing plan and a defined benefit plan for last year, even though 2021 has already ended.

Traditionally, a business owner/executive was required to start retirement plans before the end of the calendar year for which they wanted to fund the plan. Now, your clients can establish a new 2021 plan by their 2022 corporate tax return due date (including extensions).

Depending on the type of business, your client’s deadline may be extended as far out as September of 2022 (accounting for the time needed to start and fund the plan prior to October 15, 2022). Be sure to share this information with your CPA partners.

Bottom Line: If you have clients who own businesses, are sole proprietors, or are paid via 1099, we still have time to help them get large business deductions – for last year (2021)!

The Beauty of Profit Sharing and Cash Balance Plans

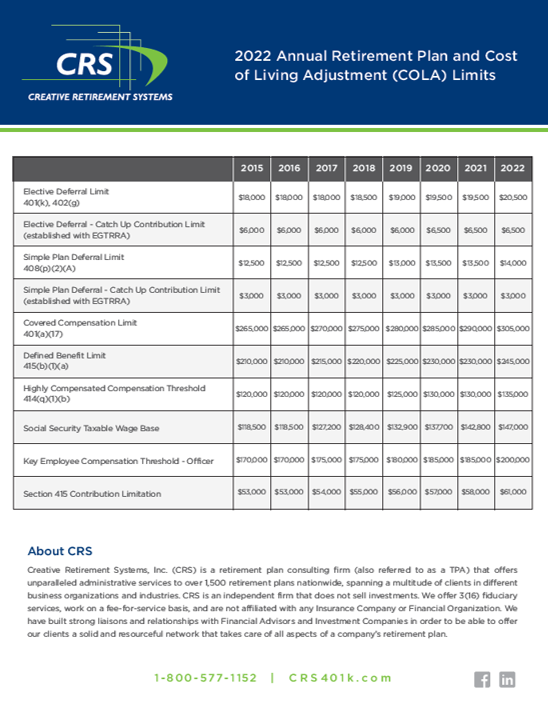

One major tax consideration for profit sharing and cash balance plans are their ability to allow significantly higher contribution amounts compared to standard 401(k) plan limits ($20,500 in 2022 401(k) deferrals for those under age 50, and $27,000 for those aged 50+).

With an existing 401(k) plan in place and depending on the design of the plan, your clients may contribute $67,500 (with the inclusion of a profit sharing plan and depending on age) and well over $250,000 (through a cash balance plan).

With the new timeline extension to sponsor such plans, your clients may wish to consider these plans as part of a broader tax mitigation solution.

Timing Considerations

Your clients can adopt a defined benefit, cash balance, and profit sharing plan for the 2021 plan year, up to the Fall of 2022 – depending on their type of business and tax filing status.

It’s important for your clients to file an extension for the 2021 tax filing season so they have adequate time to set up their new profit sharing or cash balance plan.

Who is a Good Candidate for a Profit Sharing or Cash Balance Plan?

This type of plan design tends to lend itself best to companies who are sole proprietors (with no employees) all the way up to employers with 20-30 employees.

Please contact CRS to receive specific deadlines for your individual clients and be sure to download our 2022 Retirement Plan Limits flyer here>>

Michael Davis has been in the retirement plan industry since 1994 and is our Vice President of Sales at CRS. Michael can be reached via email at .

{kind=link}