Income is Counted Very Differently for Self-Employed Individuals

Your clients look to you for guidance on making sound retirement planning decisions. And if they are small, self-employed businesses, they may be less likely to adopt an employer retirement plan.

According to data gathered by SCORE, 34% of small-business owners do not have retirement savings plans for themselves, and 40% of business owners are not confident they will be able to retire before the age of 65.*

This is interesting because – in contrast to that data — the fact that self-employed individuals don’t have any employees gives them a massive opportunity to save through retirement plans (Solo-K and Cash Balance plans). This gives you a broad prospecting pool from which to mine new business.

There is a major nuance for self-employed individuals, though: Their income is counted differently for retirement plan purposes. We frequently see CPAs and financial advisors make mistakes when projecting how much a self-employed individual can contribute to a retirement plan because they are often unaware of how plan-eligible compensation is calculated for the self-employed individual. This can create costly corrections, requiring our involvement and the intervention of an ERISA attorney to fix issues such as excess contributions for prior plan years.

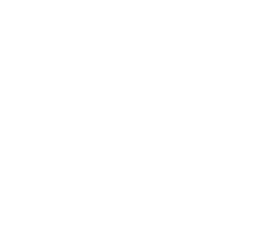

CRS has created a sales tool that helps your clients or prospects determine how much they can contribute to an owner-only 401(k) profit sharing plan – it walks you through the Earned Income Calculation. This brochure and worksheet will help empower owners and remove any confusion or fear they may have. Also, this can serve as a great entry point for discussions to gain inroads to a retirement plan sale.

This worksheet is ideal for owners with Schedule C income, no employees, and who are taxed as a sole proprietorship. In addition, this worksheet works well for partnerships where the partners are treated as “individuals,” have no employees, and who are taxed as a partnership (e.g., LLC, LLP, etc.)

Download the free brochure, Calculating Retirement Plan Contributions for Self-Employed Business Owners with No Employees, here.

Alternatively, if you prefer to have us calculate a client’s retirement plan earned income or have any questions with this worksheet, please call your local sales representative. If you aren’t sure who to call, contact us by calling 800-577-1152 (Option 2).

*Source: One-Third of Small Business Owners Lack a Retirement Savings Plan.

https://www.score.org/resource/infographic-small-business-retirement-investing-your-future

Michael Davis has been in the retirement plan industry since 1994 and is our Vice President of Sales at CRS. Michael can be reached via email at .

{kind=link}